The economic behavior system explains how decisions, habits, incentives, and structure shape financial outcomes over time.

Most people think money problems are income problems. Sometimes they are. Income matters. Wages matter. opportunity matters. Access matters. Policy matters. But income alone does not explain why some financial patterns repeat across different life stages, different jobs, different raises, and different opportunities.

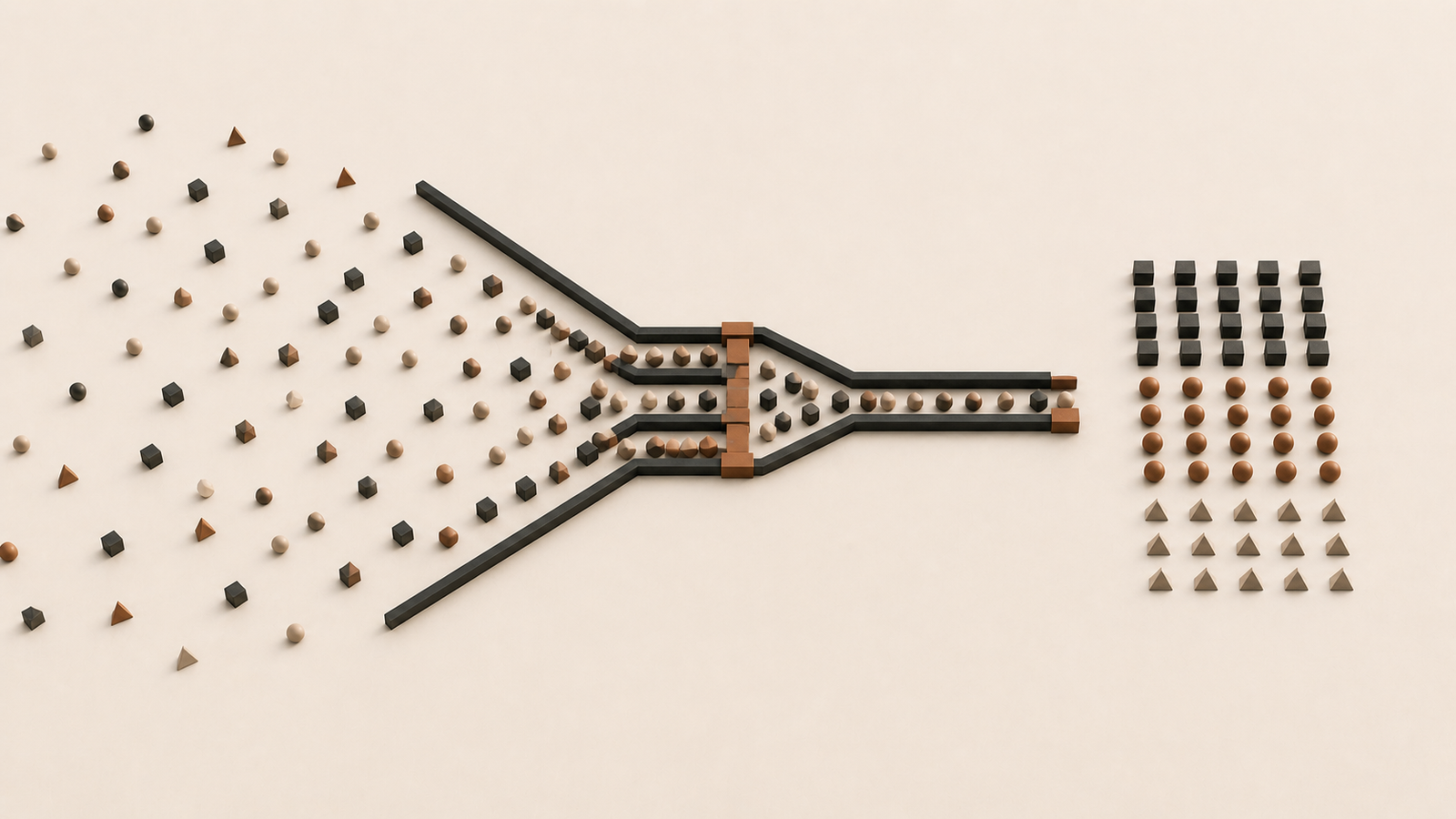

Money enters a system that already exists. That system is made of behavior.

Income enters the system once. Behavior moves through the system every day.

This is why financial outcomes cannot be understood by looking at money alone. Money follows decisions. Decisions become habits. Habits create patterns. Patterns produce outcomes. Those outcomes then reinforce the next decision.

What the Economic Behavior System Is

The economic behavior system is the interaction between incentives, decisions, habits, and outcomes that determines how money is earned, used, retained, lost, or converted into ownership.

It is not simply a money system. It is a behavior system with financial consequences.

The system includes:

- Spending patterns

- Saving behavior

- Risk tolerance

- Impulse control

- Debt response

- Attention and influence

- Reaction under pressure

- Ownership behavior

- Long-term consistency

These factors operate continuously. They do not wait for a major financial decision. They shape small choices every day, and those small choices eventually become the structure of someone’s financial life.

This is why two people can earn the same amount of money and arrive at very different outcomes. The income may be similar. The system moving the income is not.

Why Behavior Becomes Economic

Every decision has an economic dimension because every decision allocates something.

Money is one resource. But so are time, attention, energy, trust, patience, focus, and opportunity. When those resources are used without structure, financial disorder usually follows.

A person who cannot manage attention may be pulled into constant consumption. A person who cannot manage emotion may spend to regulate stress. A person who cannot manage time may miss opportunities. A person who cannot manage consistency may interrupt their own progress before it compounds.

That is why economic behavior is broader than personal finance. It is the way a person directs limited resources under real conditions.

The same logic applies to families, businesses, communities, and institutions. Every system has incentives. Every system produces decisions. Every decision creates a pattern. Every pattern produces an outcome.

The Core Misconception

The common belief is that more money creates stability.

That belief is incomplete. More money can reduce pressure, increase options, and open doors. But more money also increases exposure. It gives existing behavior more room to operate.

Without structure, increased income can lead to increased volatility. Spending rises. obligations expand. lifestyle expectations shift. The person earns more but remains under pressure because the system underneath the income never changed.

With structure, increased income can lead to increased stability. More money becomes more margin, more ownership, more capacity, and more freedom. The difference is not only the income. The difference is the behavior managing it.

The Components of the Economic Behavior System

Incentives

Incentives shape what people are encouraged to do.

A discount creates urgency. A credit offer creates access. A social environment creates comparison. A workplace creates earning patterns. A family history creates assumptions. A platform creates influence. These forces do not make every decision for a person, but they shape the field in which decisions happen.

Ignoring incentives is weak analysis. People do not make financial decisions in empty space. They make them inside systems that reward some behaviors and punish others.

Decisions

Decisions are the moments where incentives meet behavior.

A person decides whether to spend, save, wait, borrow, invest, delay, repair, compare, or walk away. Those decisions may feel isolated, but they rarely are. They usually reflect an existing pattern.

One decision can matter. Repeated decisions matter more.

Habits

Habits are decisions that have become automatic.

This is where the economic behavior system becomes powerful. Once a habit is formed, the decision no longer feels like a decision. It feels normal.

That can work for or against the person. Automatic saving builds stability. Automatic spending creates leakage. Automatic comparison creates pressure. Automatic avoidance allows problems to grow.

Outcomes

Outcomes are the visible results of invisible patterns.

Debt, savings, ownership, stress, opportunity, and financial confidence rarely appear out of nowhere. They are usually the result of repeated decisions interacting with real conditions over time.

Outcomes reveal the system. They show what has been repeated long enough to become visible.

Reinforcement

Financial outcomes reinforce behavior.

If a person spends impulsively and temporarily feels relief, the behavior may repeat. If a person saves consistently and experiences less panic, the behavior may strengthen. If debt creates stress and stress creates more spending, the loop tightens.

This is why patterns persist even when people intend to change.

The Behavior Loop

Incentives influence decisions.

Decisions become habits.

Habits shape outcomes.

Outcomes reinforce behavior.

The cycle repeats.

This loop explains why financial patterns can continue even after income changes. A raise does not automatically break the loop. A new job does not automatically break the loop. A windfall does not automatically break the loop. The behavior loop must be identified, interrupted, and redesigned.

Positive Loops and Negative Loops

The economic behavior system can work in either direction.

Positive Loop

A positive loop begins when behavior creates stability.

Structure creates spending control.

Spending control creates margin.

Margin creates savings.

Savings create confidence.

Confidence supports ownership.

Ownership expands freedom.

This is not glamorous. It is structural. The power is in repetition.

Negative Loop

A negative loop begins when behavior creates instability.

Impulse creates spending.

Spending reduces margin.

Low margin creates stress.

Stress drives short-term decisions.

Short-term decisions create debt.

Debt reinforces pressure.

Once this loop is active, more income may help, but it will not automatically solve the problem. If the behavior remains unchanged, the new income enters the same unstable system.

Why Income Does Not Break the Loop

Income enters the economic behavior system as fuel. It does not decide the destination.

If the system is disciplined, income can become stability, ownership, investment, generosity, preparation, and freedom. If the system is reactive, income can become pressure, comparison, overextension, debt, and exhaustion.

This is the reason Discipline Before Dollars exists as a core principle. Money cannot fix what behavior has not already stabilized.

More income gives behavior more consequence. It does not replace the need for structure.

Where Behavior Overrides Income

Spending

Without structure, spending follows emotion. Income increases the size of the decision, not the quality of it.

A person may earn more and still feel behind if spending expands at the same speed as income. That is not just a math problem. It is a behavior loop.

Saving

Saving behavior is not triggered by income alone. It is sustained by consistent rules and repeated action.

People who save regularly usually have a system. People who wait to save whatever is left often discover that nothing is left.

Debt

Debt often reflects behavior under pressure. Quick decisions without structure create long-term constraints.

Debt can also be structural, systemic, and tied to broader economic conditions. That matters. But even then, behavior still determines how pressure is managed, reviewed, and prevented from multiplying when possible.

Consumption

Consumption becomes dangerous when it starts functioning as identity.

If spending is used to prove success, manage insecurity, or signal belonging, money becomes attached to image. That makes restraint feel like loss instead of alignment.

Ownership

Ownership requires behavior that can hold responsibility over time.

Buying is not the same as owning. Ownership requires maintenance, patience, stewardship, and long-term thinking. Without those, ownership can become another form of pressure.

Investing

Investing works best when the behavior behind it is stable.

This is why Financial Freedom Begins Before Your First Investment is a natural application of this system. Investments can compound capital, but behavior determines whether the investor can stay with the process long enough for compounding to matter.

Economic Behavior Across a Lifetime

Economic behavior develops over time.

Children absorb financial patterns before they understand money. They watch how adults spend, argue, save, avoid, repair, share, and respond to pressure.

Young adults often inherit assumptions before they have the language to question them. Some inherit scarcity. Some inherit entitlement. Some inherit discipline. Some inherit confusion.

Families turn economic behavior into household culture. The household teaches what money means, what pressure justifies, what gets discussed, and what remains hidden.

Professionals often confront lifestyle expansion as income rises. The question becomes whether increased income creates margin or simply funds a more expensive version of instability.

Later in life, economic behavior determines whether past decisions created flexibility or constraint.

The timeline changes. The system remains active.

Institutional Economic Behavior

Individuals are not the only ones with economic behavior.

Families have economic behavior. Businesses have economic behavior. Churches, nonprofits, schools, governments, and communities have economic behavior too.

An institution reveals its economic behavior through budgeting, priorities, reserves, debt, maintenance, staffing, investment, transparency, and accountability.

A business that chases revenue without controls can scale disorder. A nonprofit that avoids financial clarity can weaken its mission. A government that spends without accountability can turn resources into distrust. A household that avoids money conversations can pass confusion across generations.

The scale changes. The loop remains.

Connection to Structure

This system sits under Structure Builds Freedom.

Structure defines the rules. Behavior follows those rules. Without structure, behavior becomes inconsistent and outcomes become unstable.

Structure is what allows economic behavior to become intentional instead of reactive.

Connection to Discipline

This system is directly tied to Discipline Before Dollars and The Discipline System.

Discipline determines whether behavior becomes consistent. Without discipline, economic behavior becomes reactive. With discipline, money has a pattern to follow.

Connection to Attention

This system also connects to The Attention Economy System.

What captures attention influences decisions. If attention is directed externally, behavior follows. If attention is structured, behavior becomes intentional.

Economic behavior is not only shaped by income. It is shaped by what people repeatedly see, compare, desire, fear, and believe they are missing.

Continue Building

Move through the framework:

Structure Builds Freedom

Why systems create the conditions for freedom.

Discipline Before Dollars

Why behavior must stabilize before resources can create freedom.

Financial Freedom Begins Before Your First Investment

Why disciplined behavior must exist before investing can become sustainable.

The Groundwork Principle

Money does not behave independently. It follows patterns of decision-making. Change the behavior, and the outcome changes with it.

Financial outcomes are not random. They are the result of repeated decisions interacting with structured or unstructured systems.

Understanding this system is the first step toward changing it.