Groundwork Framework | Economy & Ownership

Generational Wealth Architecture

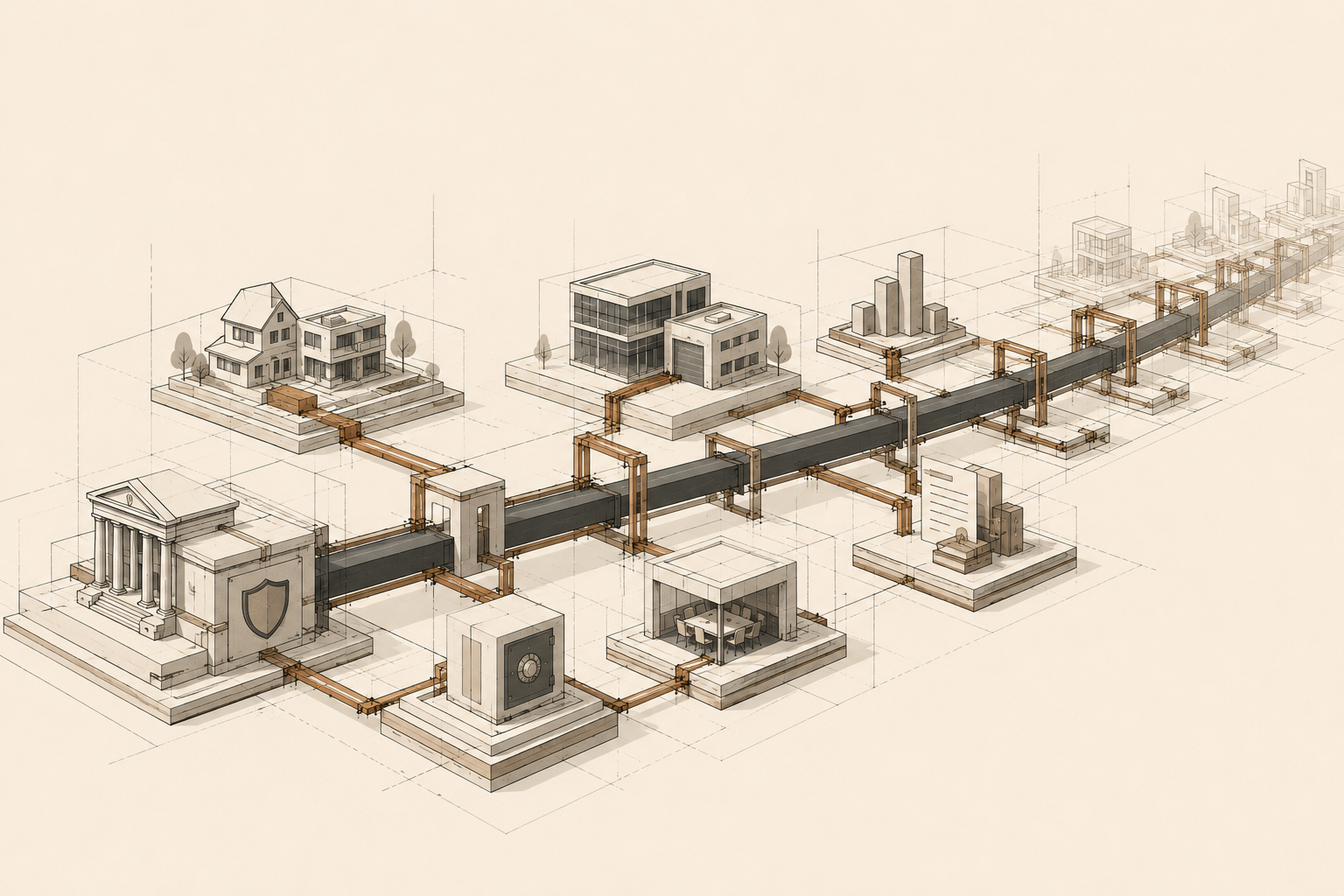

Generational wealth architecture is the system families use to build, protect, govern, transfer, and sustain wealth across generations.

Most wealth conversations are too thin. They isolate one asset, one habit, or one inspirational idea. One person says buy a home. Another says invest in stocks. Another says start a business. Another says build group economics. Each point has value, but none of them is enough alone.

Wealth becomes durable only when the pieces are connected.

A home without estate planning can become a probate problem. A business without succession planning can die with the founder. Stock ownership without emotional discipline can collapse under panic selling. Group economics without governance becomes confusion with good intentions. Starting capital without financial standards can disappear through lifestyle inflation.

That is the central lesson.

Generational wealth is not one breakthrough. It is infrastructure.

Wealth becomes generational when ownership, governance, protection, and transfer systems become stronger than individual personalities.

What Generational Wealth Architecture Means

Generational wealth architecture is the coordinated design of family stability across time.

It includes assets, but it is not limited to assets. It includes money, but it is not limited to money. It includes homeownership, investing, business equity, estate planning, land preservation, family governance, financial behavior, and long-term decision-making.

The word architecture matters.

Architecture implies design. It implies load-bearing structure. It implies sequence. It implies that one part of the system supports another.

A family that wants long-term wealth needs more than income. It needs a structure that can hold pressure.

Pressure comes in many forms:

- Job loss

- Medical emergencies

- Death

- Divorce

- Market volatility

- Business failure

- Family conflict

- Probate delays

- Property disputes

- Undocumented ownership

Weak systems collapse under pressure. Strong systems absorb pressure and continue.

That is the difference between wealth that appears and wealth that lasts.

Why Wealth Needs Architecture

Wealth without architecture is exposed.

A person can earn a good salary and still build nothing durable. A household can buy a home and still have no liquidity. A family can inherit land and still lose it through unclear title. A founder can build a profitable business and still leave no structure for the next generation.

That is not a money problem alone. It is a systems problem.

Most families do not lose wealth in one dramatic collapse. They lose it through leakage.

Leakage looks like:

- Unplanned emergencies

- High-interest debt

- Lifestyle inflation

- No insurance

- No estate plan

- No successor preparation

- No investment habit

- No family financial standard

- No legal documentation

- No shared understanding of ownership

Architecture closes the leaks.

It turns scattered effort into a system. It gives money assignments. It gives assets protection. It gives heirs clarity. It gives family members standards. It gives the next generation a better starting point.

That is the work.

Pillar 1: Ownership

Ownership is the first structural layer of generational wealth architecture.

Income pays for life. Ownership changes the family’s position inside the economy.

Ownership can include:

- Homes

- Land

- Businesses

- Stock portfolios

- Retirement accounts

- Intellectual property

- Tools and equipment tied to skilled labor

- Revenue-producing systems

However, ownership must be real. A car with a large payment is not wealth. A house with no maintenance plan is fragile. A business with no books is unstable. Family land with unclear title is vulnerable.

Ownership must be maintained, protected, documented, and transferable.

That is why the architecture matters. It is not enough to acquire an asset. The family must know how the asset works, what it costs, who controls it, how it grows, how it is protected, and how it transfers.

Without that structure, ownership becomes symbolic.

With structure, ownership becomes leverage.

Pillar 2: Protection

Protection is the defensive layer.

Too many wealth conversations start with growth. That is backward. Wealth that is not protected cannot compound safely.

Protection includes:

- Emergency savings

- Health insurance

- Life insurance

- Property insurance

- Business insurance

- Estate planning

- Legal documents

- Beneficiary reviews

- Clear title

- Tax preparation

Protection is not pessimism. It is maturity.

A family that refuses to plan for disruption is not being optimistic. It is being exposed.

Every family building wealth should ask:

- What happens if the main income earner dies?

- What happens if someone becomes disabled?

- What happens if the property needs major repairs?

- What happens if heirs disagree?

- What happens if the business owner exits suddenly?

- What happens if the market drops?

- What happens if one person wants to sell a shared asset?

If the answer is “we will figure it out,” the system is weak.

Wealth requires protection before expansion.

Pillar 3: Investment

Investment is the compounding layer.

Labor matters. Skill matters. Work matters. Still, labor alone has limits. People age. Jobs change. Industries shift. Health changes. Family obligations increase.

Investment allows money to work beyond direct labor.

Investment systems may include:

- Employer retirement plans

- Individual retirement accounts

- Brokerage accounts

- Index funds

- Dividend-producing assets

- Business reinvestment

- Education savings

- Long-term property improvement

The key is consistency.

Investment is not supposed to be emotional theater. It should not be trend chasing, panic buying, panic selling, or trying to look smart online. It should be boring, disciplined, and tied to a long-term strategy.

This is especially important for families that have not historically had broad access to investment systems. Market participation requires trust, education, emotional regulation, and patience.

Those qualities are not automatic. They must be taught.

Pillar 4: Governance

Governance determines whether wealth survives human behavior.

This is the section most financial content skips. That is a mistake.

Families do not lose wealth only because of bad markets. They lose wealth because of unclear expectations, poor communication, weak documentation, emotional decision-making, and conflict.

Governance creates order.

Family governance can include:

- Annual family financial reviews

- Clear decision authority

- Written agreements for shared assets

- Defined roles for property management

- Rules for selling inherited assets

- Business succession plans

- Conflict resolution standards

- Education for younger family members

- Shared expectations around debt and support

Governance is not cold. It is protective.

Families often confuse love with informality. That is dangerous. Love does not replace documents. Trust does not replace clarity. Good intentions do not prevent future conflict.

Governance protects relationships by removing confusion before pressure arrives.

Pillar 5: Psychology

Families transfer more than money.

They transfer behavior.

They transfer urgency, fear, discipline, avoidance, trust, suspicion, patience, and emotional regulation. They transfer ideas about what money is for, what risk means, whether institutions can be used, and whether the future is worth planning for.

This is generational wealth psychology.

A family shaped by instability may teach caution without naming it. That caution may protect people from reckless choices. However, it may also block investment, business ownership, estate planning, and long-term strategy.

A family shaped by stability may teach patience as normal. Children may watch adults save, invest, insure, negotiate, plan, and document. Those behaviors become familiar before adulthood.

That familiarity is a form of capital.

Psychology matters because systems require behavior to maintain them. A family can create a budget and ignore it. A family can open an investment account and panic during volatility. A family can write a will and never update it. A family can inherit property and fight over it.

Structures fail when behavior cannot carry them.

Therefore, emotional regulation is part of wealth architecture.

Pillar 6: Transfer

Transfer is where wealth becomes generational.

Many families build assets. Fewer families transfer them cleanly.

Transfer systems include:

- Wills

- Trusts

- Beneficiary designations

- Clear property title

- Business succession plans

- Life insurance instructions

- Estate inventories

- Digital access plans

- Document storage systems

- Successor education

Transfer is not only about who gets what.

It is about whether the asset survives the transition.

A property can be valuable and still become trapped in probate. A business can be profitable and still collapse without successor authority. Land can be emotionally important and still be lost through heirs’ property fragmentation. Investment accounts can exist and still be delayed because beneficiaries were never updated.

Transfer requires design.

Without transfer systems, every generation starts over too much.

Why Wealth Disappears

Wealth often disappears quietly.

It does not always vanish because someone made one terrible decision. More often, it leaks through repeated small failures that were never governed.

Common failure points include:

- Fragmentation: too many heirs, no clear authority, no shared plan.

- Consumption pressure: money used to perform success instead of build stability.

- Legal neglect: no will, no trust, no title clarity, no beneficiary review.

- Underinsurance: one death, illness, or disaster destabilizes the entire household.

- Weak financial literacy: heirs receive assets without understanding responsibility.

- Conflict: emotional disputes destroy what documents could have protected.

- No successor preparation: businesses and properties depend on one person only.

- Short time horizons: immediate pressure overrides long-term compounding.

The lesson is simple.

Assets do not preserve themselves.

Families must build continuity on purpose.

The Complete Reading Pathway

This page is the central map. The full framework below moves through the major systems families need to understand, build, and protect.

How to Build Generational Wealth as a Black Family

The full anchor article connecting the wealth-building system into one family operating framework.

Protection and continuity

Estate Planning Is Infrastructure

Shows why wills, trusts, beneficiaries, and legal planning protect wealth from confusion and breakdown.

Heirs’ Property and Black Land Loss

Explains how unclear title and fragmented ownership can destroy land transfer across generations.

Investment and compounding

Why Stocks Matter for Black Wealth

Explains why long-term equity ownership matters beyond wages and homeownership.

Why Starting Capital Changes Everything

Shows how unequal starting positions shape risk, recovery, opportunity, and compounding.

Ownership and leverage

Homeownership Alone Cannot Close the Gap

Explains why housing matters but cannot carry the full wealth-building burden alone.

Business Ownership Is a Wealth Multiplier

Frames business equity as a scalable asset beyond individual labor.

Systems and governance

The Hidden Cost of Appraisal Bias

Breaks down how undervaluation limits equity, leverage, borrowing power, and long-term asset growth.

Group Economics Without Fantasy Thinking

Separates serious cooperative economics from slogans by focusing on governance and accountability.

Behavior and time horizon

Generational Wealth Psychology

Explains how families transfer habits, scarcity patterns, emotional responses, and financial behavior.

Where to Start

If a family wants to build generational wealth, the first move is not to chase every asset at once.

The first move is sequence.

- Stabilize the household. Know the budget, debt, income, obligations, and emergency exposure.

- Protect the household. Put insurance, beneficiaries, wills, and basic documents in place.

- Build ownership. Acquire assets that can appreciate, produce income, or reduce dependency.

- Create investment habits. Build long-term compounding systems that do not depend only on labor.

- Govern the assets. Create roles, agreements, reviews, and standards.

- Prepare transfer. Make sure the next generation receives structure, not confusion.

- Teach the operating system. Transfer knowledge before transferring control.

That is the architecture.

Not hype. Not fantasy. Not performance.

Structure.

Receipts

Federal Reserve: Survey of Consumer Finances

The Federal Reserve tracks household wealth, asset ownership, debt, retirement accounts, and racial wealth gaps.

Read the Federal Reserve SCF data

FDIC: National Survey of Unbanked and Underbanked Households

The FDIC tracks bank account access, financial inclusion, and alternative financial service use across households.

Read the FDIC household banking survey

Fannie Mae: Heirs’ Property Research

Fannie Mae explains how heirs’ property affects ownership stability and home equity preservation.

Read the Fannie Mae heirs’ property report

Urban Institute: Estate Planning and Tangled Titles

Urban Institute research explains how unclear property ownership can threaten wealth preservation.

Read the Urban Institute report

National Consumer Law Center: Heirs’ Property

NCLC outlines how heirs’ property can create forced-sale risk and undermine wealth retention.

Read the NCLC heirs’ property report

FAQ

What is generational wealth architecture?

Generational wealth architecture is the coordinated system families use to build, protect, govern, transfer, and sustain wealth across generations.

Why is generational wealth more than money?

Generational wealth includes assets, but it also includes knowledge, habits, legal documents, ownership systems, governance, protection, and successor preparation.

What is the first step in building generational wealth?

The first step is household stability. A family should understand its income, expenses, debt, emergency exposure, and basic protection needs before expanding into larger wealth-building moves.

Why does estate planning matter?

Estate planning protects assets from probate confusion, family conflict, unclear transfer, and unnecessary loss. It turns inheritance into a managed process instead of a crisis.

Why is family governance important?

Family governance creates rules, expectations, documentation, and decision-making standards. It helps wealth survive conflict, transition, and leadership change.

Can homeownership alone create generational wealth?

Homeownership can support wealth-building, but it is not enough alone. Families also need liquidity, insurance, investment habits, estate planning, and clear title.