Operating vs Capital Budgets: How Cities Allocate Power

Operating vs capital budgets determine how cities allocate power, maintain services, and invest in long-term infrastructure. Although both appear in the same municipal budget, they follow different structural rules. Understanding the distinction clarifies why some cities feel stable while others feel perpetually under repair.

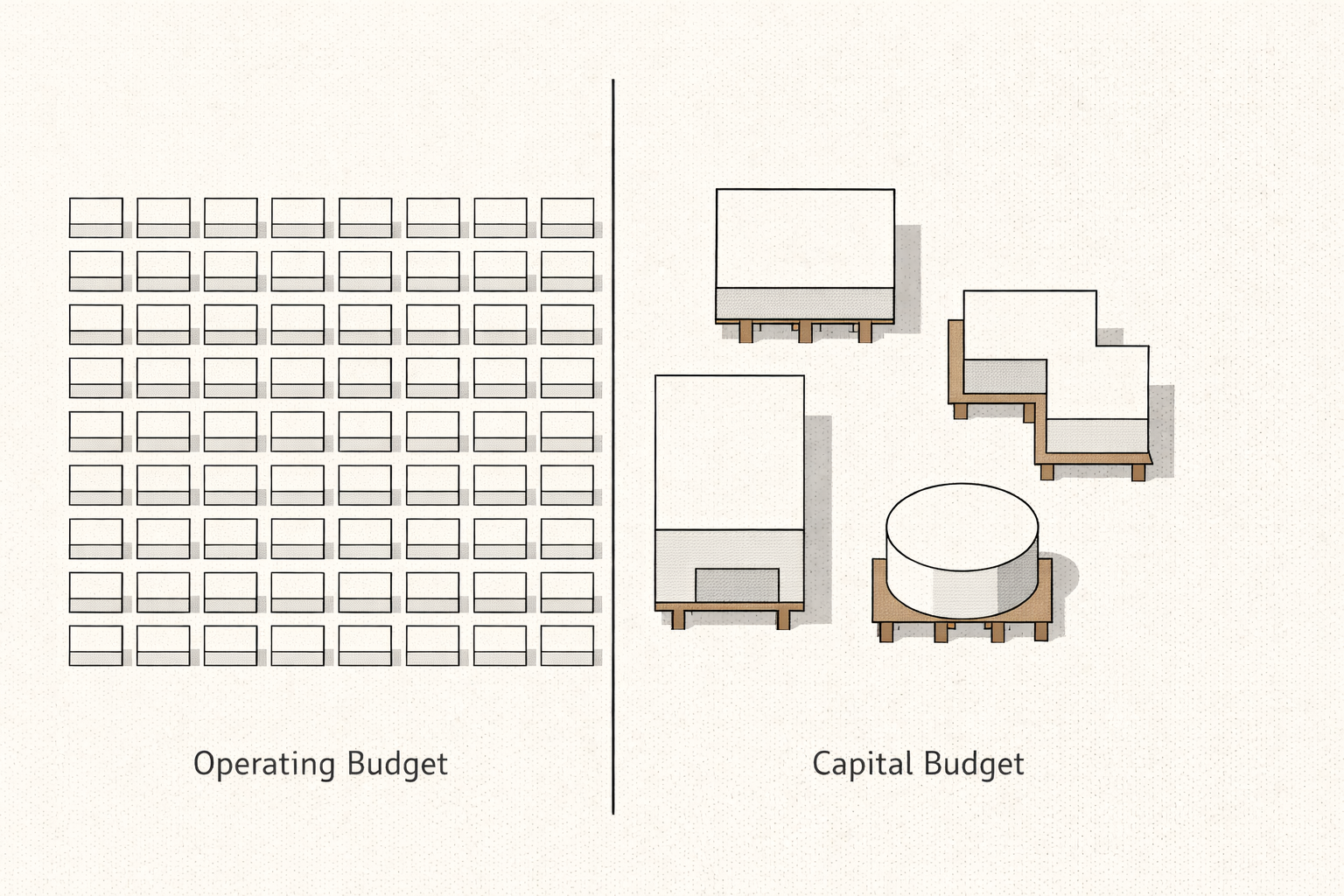

Operating vs Capital Budgets: What Is an Operating Budget?

An operating budget funds recurring, day-to-day obligations. It pays for staff, utilities, sanitation routes, classroom operations, inspections, and routine maintenance. Because these expenses repeat every fiscal year, operating budgets require reliable revenue that repeats as well.

In practice, operating discipline shapes daily civic experience. When leaders freeze hiring, cap overtime, or reduce service hours, those choices hit the operating side first. As a result, residents feel the change immediately through slower response times, reduced access, or weakened continuity.

Operating vs Capital Budgets: What Is a Capital Budget?

A capital budget funds long-term public assets. Roads, bridges, transit systems, school construction, major building rehabilitation, and water infrastructure typically sit inside capital planning. Unlike operating expenses, these projects span multiple years and require upfront investment.

Therefore, capital budgets often rely on long-term financing such as bonds. This approach can be responsible when it matches the lifespan of the asset. However, borrowing becomes a problem when debt service grows faster than the city’s capacity to sustain it.

Most municipalities separate operating and capital expenditures using public finance standards promoted by the Government Finance Officers Association. That separation reduces the risk of financing everyday services with long-term debt.

Why Operating vs Capital Budgets Matter for Civic Stability

The difference between operating vs capital budgets is not accounting trivia. Instead, it is structural governance.

Operating spending sustains what already exists. Capital spending expands, replaces, or repairs physical systems. Consequently, leaders constantly choose between immediate continuity and long-range durability.

When operating costs rise faster than recurring revenue, leaders cut services or raise taxes. When capital investment lags, infrastructure degrades and emergency repairs become routine. Meanwhile, excessive borrowing increases debt service and pressures future operating flexibility.

How Operating vs Capital Budgets Reveal Public Priorities

Every allocation reflects trade-offs. For example, expanding transit may limit room for staffing growth. Funding housing rehabilitation may reduce capacity for new construction. Increasing wages may delay capital upgrades. Because choices compete inside the same budget environment, priorities become visible quickly.

Operating vs capital budgets also reveal whether a city values maintenance or visibility. A city can announce major capital projects while underfunding routine upkeep. Conversely, a city can protect operating payroll while deferring infrastructure until failure forces expensive replacement. Either way, the budget tells the truth.

Operating vs Capital Budgets and Voter Responsibility

When citizens vote, they influence who manages operating vs capital budgets. They select allocation managers, not speechwriters. Therefore, civic literacy requires one basic question before any debate: is this proposal an operating obligation or a capital investment?

Next, follow the financing. Does the initiative rely on recurring revenue, temporary funds, or long-term debt? The answer determines whether the policy strengthens stability or creates future strain.

Operating budgets keep the city functioning. Capital budgets shape the city’s future form. When both are funded with discipline, services remain reliable and infrastructure performs as designed. When discipline fails, structural weakness hides beneath clean ledgers.