Financial stability is engineered, not earned. Income matters, but structure determines whether money becomes security or pressure.

Most people assume financial stability begins when income rises. That assumption is understandable. However, it is incomplete.

Higher income can create more options. Even so, more money does not automatically create order. Without financial systems underneath it, additional income often increases exposure. Expenses expand. Lifestyle expectations rise. Debt becomes easier to justify. Eventually, pressure grows beneath the surface.

For that reason, financial stability systems matter. They determine whether income builds security or collapses under pressure.

Income is fuel. Infrastructure is containment. Without containment, fuel creates fire.

What Financial Stability Really Means

Financial stability is not the same as having money in the moment. Instead, it is the ability to remain steady when life creates friction.

A stable financial life has structure before stress arrives. Bills are visible. Savings are automated. Emergency reserves are separate. Debt has limits. Spending has boundaries. As a result, decisions do not depend on mood, panic, or motivation.

That is the difference between earning money and engineering stability.

One is income. The other is architecture.

Why Income Alone Does Not Create Stability

Income solves some problems. Still, it does not solve disorganization.

A person can earn more and remain financially unstable if every dollar is already assigned to pressure. Rent rises. Subscriptions multiply. Credit balances grow. Convenience becomes normal. Then emergencies become debt events instead of contained disruptions.

This is how people with decent incomes still feel financially cornered.

Often, the problem is not earning power. The problem is load distribution.

Without structure, income flows toward whatever is loudest. Bills get paid late. Savings happen only when money is left over. Unexpected costs become emergencies. Therefore, progress resets after disruption.

That is not only a money problem. It is a system problem.

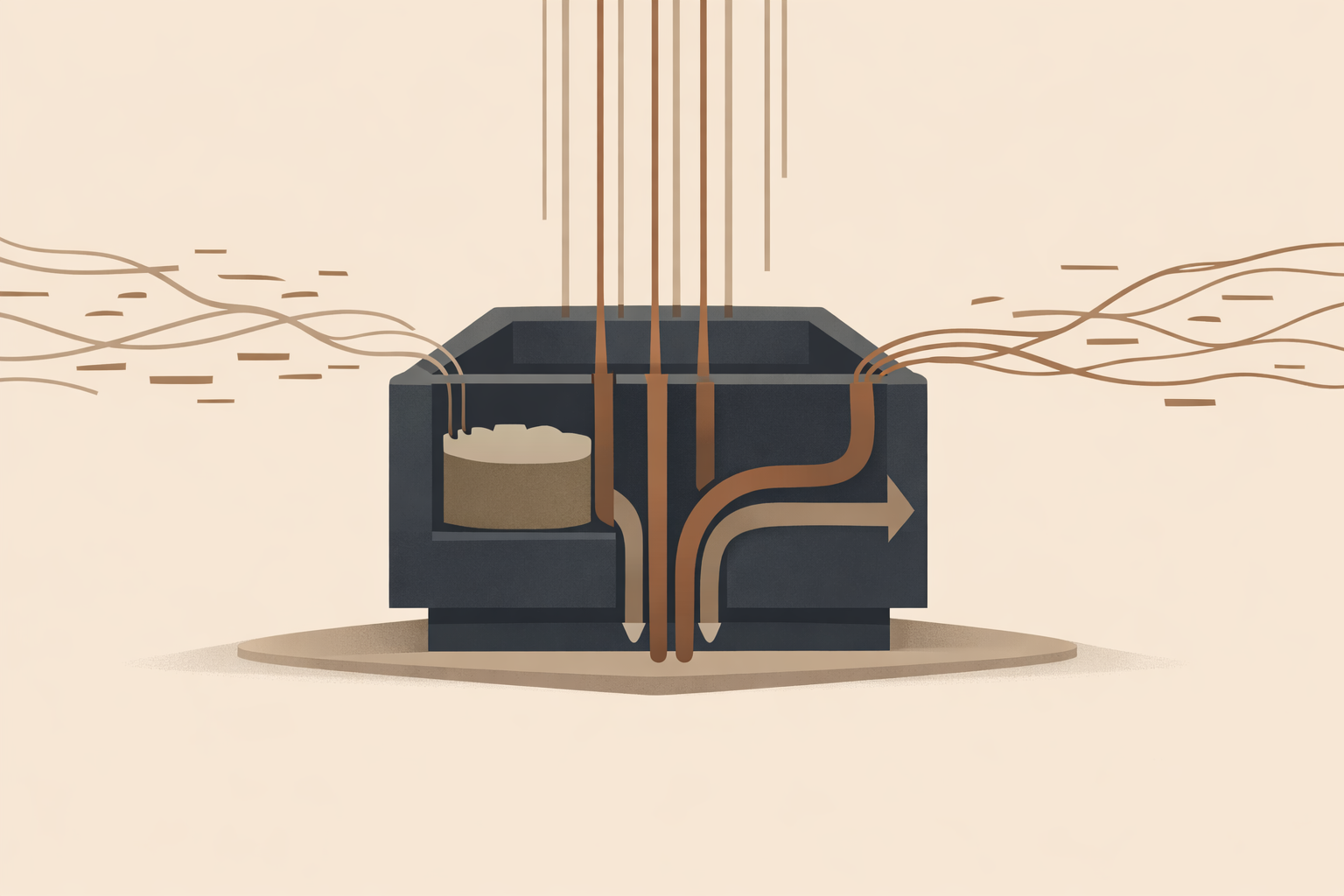

Financial Stability Systems Are Load-Bearing Beams

A budget is not punishment. It is reinforcement.

Inside a building, a load-bearing beam does not exist for decoration. It carries weight. It keeps pressure from concentrating in weak areas. Because of that, the structure can hold when conditions change.

Your financial systems serve the same purpose.

They carry the weight of daily choices before those choices become emotional. They also protect the household from volatility. More importantly, they keep one surprise expense from damaging the whole structure.

Without financial stability systems:

- Income expands expenses automatically.

- Unexpected costs trigger emotional decisions.

- Debt becomes the pressure release valve.

- Progress resets after disruption.

- Stress remains high even when income improves.

With financial stability systems:

- Income has direction.

- Spending has boundaries.

- Savings happen before convenience spending.

- Emergency buffers absorb shock.

- Growth has a floor beneath it.

This difference is not motivational. It is structural.

The Core Financial Stability Systems

Financial stability does not require a complicated setup. Instead, it requires systems that repeat without needing emotional energy every time.

1. A Fixed-Cost Ceiling

The first system is a ceiling on fixed expenses. Housing, transportation, insurance, utilities, subscriptions, debt payments, and other recurring costs must remain visible.

When fixed costs rise too high, flexibility disappears. Every paycheck becomes pre-committed before it arrives. Consequently, financial fragility can exist even when income looks healthy on paper.

As a working standard, fixed expenses should stay below 60% of take-home pay whenever possible. That gives the rest of the system room to breathe.

2. Automated Savings

Savings should not depend on leftover money. Leftover money is too fragile.

Automation protects savings from impulse, fatigue, and forgetfulness. The transfer happens before discretionary spending begins. In practice, that turns savings from an intention into an operating rule.

The amount can start small. At first, the structure matters more than the number.

3. A Separate Emergency Buffer

An emergency fund is not extra cash. It is shock absorption.

The fund should sit outside the daily spending flow. It should be liquid, accessible, and boring. Its purpose is not growth. Its purpose is protection.

A three-month emergency buffer is a strong baseline. However, more may be needed if income is irregular, dependents rely on the household, or major obligations are already in place.

4. Debt Boundaries

Debt becomes dangerous when it turns into a lifestyle stabilizer.

Credit should not be the system that keeps daily life operational. When debt fills every gap, the household is not stable. Instead, it is borrowing against future capacity to protect present comfort.

Clear debt boundaries create discipline before pressure becomes normal.

5. Quarterly Net Worth Review

Daily balance checking can create anxiety without strategy. By contrast, a quarterly net worth review gives a clearer signal.

The question is not only, “How much money is in the account?”

The better question is, “Is the structure getting stronger?”

Assets, liabilities, savings rate, debt direction, and emergency reserves tell the real story.

What Happens Without Financial Stability Systems?

When financial stability systems are absent, stress increases even during income growth.

Unexpected expenses feel catastrophic. Lifestyle creep accelerates. Debt becomes normal. Meanwhile, financial anxiety stays present because the person is not living inside a protected structure.

This is why some people earn more and still feel behind.

The income changed. The operating system did not.

Financial pressure also affects decision-making. Stress narrows attention. It makes short-term relief feel more urgent than long-term protection. As a result, every problem demands emotional labor when the system is weak.

→ American Psychological Association — Stress

→ Federal Reserve — Economic Well-Being of U.S. Households

How to Engineer Financial Stability

Financial stability is built through sequence. Therefore, the order matters.

Do not start with investment complexity. Do not start with lifestyle upgrades. Also, do not start with the fantasy version of the future.

Start with containment.

- List every recurring obligation. Make the fixed-cost load visible.

- Set a fixed-cost ceiling. Keep recurring expenses from consuming the system.

- Automate savings first. Protect money before convenience spending begins.

- Build a three-month emergency buffer. Create shock absorption.

- Reduce unstable debt. Stop using debt as a lifestyle bridge.

- Review net worth quarterly. Measure structural strength, not daily noise.

This is not glamorous. That is the point.

Stability is quiet until it is needed.

Financial Stability Comes Before Financial Freedom

Financial freedom is not the first step. It is the result of enough stability, discipline, and leverage compounding over time.

Before investment, stability.

Before leverage, containment.

Before scaling, reinforcement.

Ambition without structure creates fragility. However, financial stability systems create a base strong enough to support expansion.

This is why Discipline Before Dollars remains foundational. Discipline builds beams before dollars attempt to decorate the structure.

It also aligns with Stability Is a Requirement. Growth depends on load-bearing capacity.

Likewise, Structure Builds Freedom shows why freedom expands only when systems reduce chaos.

The Bottom Line

Financial stability is not proof that life became easy. It is proof that the structure became stronger.

Income may start the engine. Systems determine whether the vehicle stays on the road.

Build the budget. Automate the savings. Protect the emergency buffer. Control the fixed costs. Then review the structure before pressure reveals the weak spots.

That is how financial stability becomes engineered, not merely hoped for.

This article is part of the Stability Framework, which moves from personal structure to emotional regulation, physical baseline control, financial containment, civic trust, and community resilience.

Stability moves from the individual to the institution. Each layer reinforces the next.

- Stability Is a Requirement, Not a Request

- Emotional Stability Is a Discipline

- Physical Stability and the Nervous System

- Financial Stability Is Engineered, Not Earned (You Are Here)

- Civic Stability and Institutional Drift

- Community Stability and Shared Responsibility

→ Discipline Before Dollars

→ Financial Stability Systems: Build the Beam Before You Build Wealth

→ Stability Is a Requirement

→ Structure Builds Freedom

Financial Stability FAQ

What does financial stability mean?

Financial stability means having systems that keep money predictable under pressure. It includes visible expenses, automated savings, emergency reserves, debt boundaries, and repeatable review habits.

Why does income alone not create financial stability?

Income alone does not create financial stability because money without structure usually flows toward expenses, convenience, and pressure. Stability requires systems that direct, retain, and protect income.

What are financial stability systems?

Financial stability systems are repeatable structures that reduce financial volatility. They include budgets, savings automation, emergency funds, fixed-cost ceilings, debt limits, and net worth reviews.

How do I start building financial stability?

Start by listing recurring expenses, setting a fixed-cost ceiling, automating savings, building an emergency buffer, reducing unstable debt, and reviewing net worth quarterly.

Is financial stability more important than financial freedom?

Financial stability comes first. Financial freedom requires a strong base. Without stability, growth becomes fragile and leverage becomes risky.