Who owns the neighborhood is not a sentimental question. It is an economic question.

Most people describe a neighborhood by what they can see. They name the grocery store, the pharmacy, the apartments, the bank branch, the corner restaurant, the vacant lot, and the old storefront that somehow survived every rent increase.

That visible layer matters. However, it is not the whole economy.

A neighborhood also has an invisible layer. Land records, commercial leases, mortgage debt, property owners, franchise agreements, supplier contracts, banking relationships, insurance costs, tax assessments, corporate entities, outside investors, and local institutions all shape what happens after money moves.

Two neighborhoods can look almost identical from the sidewalk and operate very differently underneath.

One neighborhood may circulate money through local owners, local employers, local contractors, and local institutions. Another may generate activity while most of the ownership sits somewhere else.

That difference determines whether money becomes community wealth or simply passes through.

Power & Price principle: A neighborhood is not only where people live. It is a structure of ownership, control, access, and extraction.

Who Owns the Neighborhood?

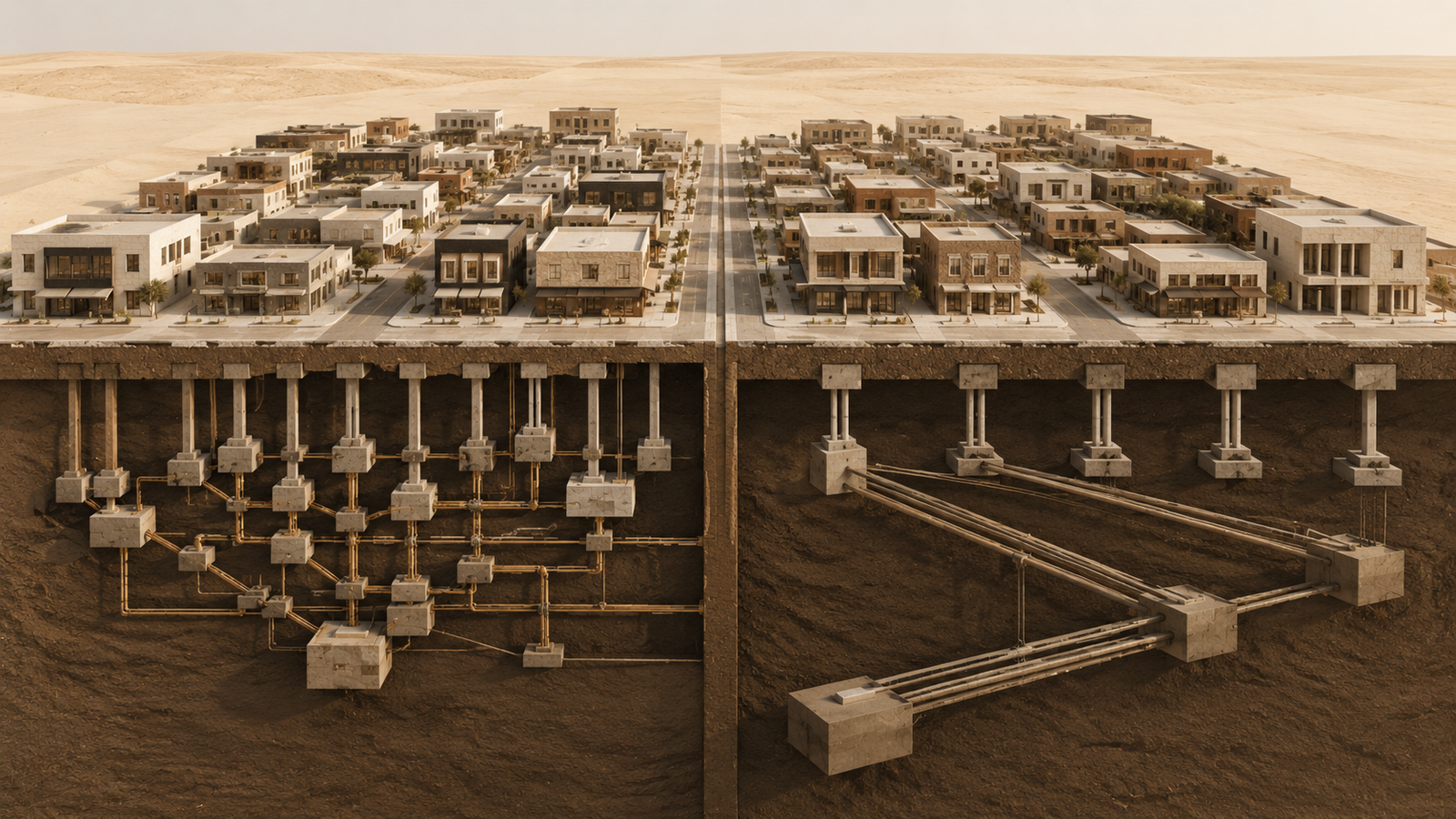

Who owns the neighborhood sounds like a simple question. It is not.

Ownership rarely sits in one place. A building may have one owner. The business inside it may have another. The land may be held through a company. The debt may be held by a lender. The brand may belong to a franchise parent. The inventory may be financed. The payment system may belong to a platform.

From the street, it looks like one business. Underneath, it may be a stack of claims.

The customer sees the store. The economy sees the structure.

This is why Spending Is Not Ownership had to come first. Spending explains movement. Ownership explains position.

Once money leaves a customer’s hand, it travels through systems. Some of it pays workers. Some of it pays suppliers. Some of it pays rent. Some of it pays debt. Some of it becomes profit. Some of it stays near the neighborhood. Some of it leaves immediately.

The ownership question asks where that value lands.

Why Who Owns the Neighborhood Changes Everything

Who owns the neighborhood matters because ownership determines leverage.

A busy street can fool people. Activity looks like strength. A commercial corridor with full storefronts, delivery trucks, and steady foot traffic can appear healthy. Still, activity alone does not tell us who is gaining power.

The street shows transactions. The balance sheet shows accumulation.

If most businesses rent from absentee landlords, the neighborhood may generate strong rent income without building local property wealth. If most stores depend on outside suppliers, the neighborhood may support demand without controlling supply. If most financing comes from outside institutions, the neighborhood may carry debt without building local lending power.

That does not mean outside ownership is automatically wrong. That would be lazy thinking.

Outside capital can bring investment, services, jobs, and stability. Local ownership can also be irresponsible, extractive, or poorly managed. Therefore, the issue is not simply local good, outside bad.

The issue is leverage.

Who can decide what stays? Who can absorb a downturn? Who captures rising value? Who has the power to renew, sell, raise rent, close, expand, or reinvest?

Those questions reveal the real economy beneath the storefront.

Commercial Real Estate Shapes Community Wealth

Commercial real estate ownership is one of the most powerful forces in neighborhood economics.

It controls location, cost, access, and who can remain when a neighborhood becomes valuable.

A business owner who does not own the building may build demand for a corridor but still remain vulnerable to rent increases. A restaurant may become a local anchor and still lose its lease. A small shop may serve residents for twenty years and still disappear when the property changes hands.

The business created value. However, the property owner may capture much of it.

This is not a moral accusation. It is how the structure works.

Land and buildings hold power because they remain after each transaction ends. They can appreciate. They can secure loans. They can generate rental income. They can be sold, inherited, refinanced, or leveraged.

That is why ownership of commercial real estate changes the future of a neighborhood.

When local residents, community institutions, cooperatives, churches, nonprofit development corporations, or mission-aligned investors own property, the neighborhood has more tools. It can negotiate from a stronger position. It can preserve space for needed services. It can resist some forms of displacement. It can make long-term decisions instead of reacting to every market shift.

When no local actor owns meaningful property, the neighborhood depends on the decisions of others.

Dependency is not stability.

Businesses Matter. Property Still Matters More.

People often talk about supporting local businesses. That matters.

However, a local business without property control can be fragile. It may have loyal customers, strong reputation, and steady revenue. Still, if the lease is weak or the rent rises beyond the model, the business can disappear.

Ownership of the business and ownership of the building are different forms of power.

A business owner controls operations. A property owner controls place.

When those roles are separated, the business owner may create community value while the property owner controls long-term leverage.

This is why a neighborhood can be full of beloved businesses and still be economically vulnerable.

The emotional map and the ownership map may not match.

A community may feel attached to a corner store, barbershop, bakery, restaurant, or childcare center. Yet if the building is owned elsewhere, attachment does not guarantee continuity.

Affection is not a lease. Memory is not ownership.

Community value needs legal and financial structure if it is going to survive market pressure.

Local Economy Means More Than Local Spending

A local economy is not created simply because people spend money nearby. That is a weak definition.

A stronger local economy includes local ownership, local hiring, local contracting, local lending, local institutions, and local decision-making power.

Spending nearby may be the beginning. It is not the finish.

Money spent in a neighborhood can still leave quickly. Rent may go to an out-of-state owner. Franchise fees may go to a parent company. Supplier payments may leave the region. Debt payments may go to distant lenders. Platform fees may go to technology companies. Insurance payments may go elsewhere.

Again, none of this is automatically wrong. But it proves the point.

Geography alone does not determine economic benefit. Structure does.

This is why the Economic Behavior System is useful beyond personal finance. It reminds us that outcomes are produced by repeated decisions inside larger incentive structures.

A community’s spending behavior matters. However, the system receiving that spending matters just as much.

The Ownership Map Is Usually Hidden

Most people do not know who owns the buildings around them.

They know the signs, the staff, the menu, the hours, and the places that treat them well. They also know which places treat them like a problem.

However, they usually do not know the ownership map.

That map is often buried in public records, business filings, leases, mortgages, corporate structures, and property databases. It may be legal, visible, and technically available while remaining practically invisible to ordinary residents.

This invisibility matters because power hides well behind routine.

A neighborhood may debate whether a new store is good or bad without knowing who owns the land. Residents may argue about rising prices without understanding rent pressure. People may blame one business for closing without seeing debt, insurance, payroll, lease renewal, or supplier costs.

The visible event gets the emotion. The hidden structure creates the condition.

Power & Price exists to name that hidden structure.

Anchor Businesses Change Neighborhood Gravity

Every neighborhood has anchors.

Some are obvious. Grocery stores, banks, schools, health clinics, pharmacies, churches, cultural spaces, and community centers shape daily life.

Others are less visible. A family-owned building, a local contractor, a childcare provider, a credit union, a commercial kitchen, or a landlord willing to preserve affordable storefront space can all become quiet anchors.

Anchors matter because they shape the flow of daily life.

A grocery store does more than sell food. It affects travel time, health, employment, commercial traffic, and neighborhood convenience. A bank does more than hold deposits. It affects credit access, financial habits, and small business formation. A school does more than educate children. It shapes family routines, civic networks, and neighborhood stability.

This is why Grocery Stores Matter More Than Grocery Stores belongs in this conversation. Certain businesses become infrastructure because they organize daily behavior around them.

When anchor institutions are locally accountable, they can strengthen community wealth.

When they are purely extractive, they can drain value while still meeting basic needs.

That is the tension.

Who Owns the Neighborhood When Capital Leaves?

Who owns the neighborhood becomes even more important when capital leaves quietly.

Capital flight sounds like a crisis. Often, it is quieter than that.

It can happen through ordinary payments repeated over time. Rent leaves. Profits leave. Interest leaves. Vendor payments leave. Insurance premiums leave. Platform fees leave. Franchise fees leave. Management fees leave.

A single payment may not look like much. The pattern matters.

When most economic value leaves a neighborhood after each transaction, the neighborhood may remain active but undercapitalized. It may have businesses but weak ownership. It may have consumers but few investors. It may have workers but few employers with local roots.

Capital flight is not only about money disappearing.

It is about decision-making leaving with it.

Once value leaves, control often leaves too.

Community Wealth Requires Institutions

Individual ownership matters. However, community wealth cannot depend only on individual heroes.

That is another weak idea.

A strong neighborhood economy needs institutions that can hold assets, manage risk, train owners, finance projects, preserve land, and coordinate trust over time.

That may include community development financial institutions, credit unions, land trusts, merchant associations, cooperative ownership models, local investment funds, nonprofit developers, churches with property discipline, and schools connected to workforce pathways.

Institutions matter because they outlast moods.

They can carry memory, hold property, set standards, pool risk, and protect continuity when individual circumstances change.

This is where Discipline Before Dollars becomes more than a personal principle. Money without institutional discipline leaks. Community ambition without legal and financial structure becomes another speech.

We do not need more slogans about ownership.

We need containers that can hold it.

Ownership Without Accountability Can Still Harm a Neighborhood

Ownership is powerful. But it is not automatically virtuous.

A local owner can neglect property. A local landlord can overcharge. A local business can mistreat workers. A local institution can become closed, political, or self-protective. A community development project can claim public purpose while serving private convenience.

Ownership must be paired with accountability.

Otherwise, it becomes another form of extraction.

This point matters because economic conversations often romanticize local ownership. That romance does not help. A bad structure remains bad even when the owner is familiar.

The better standard is not simply who owns.

It is how ownership behaves.

Does it maintain the asset? Does it hire fairly? Does it reinvest? Does it communicate honestly? Does it build trust? Does it preserve community function? Does it create pathways for others?

Ownership should create responsibility, not just status.

Why Neighborhood Change Feels Personal

Neighborhood change often feels personal because place carries memory.

People attach life to streets. First jobs, school walks, family errands, barbershop conversations, church routes, corner stores, block parties, funeral repasts, and cafés can hold entire chapters of ordinary life.

Then the rent changes. The store closes. The building sells. The new sign goes up.

The neighborhood is still there, but something has shifted.

People often describe that shift culturally. They say the neighborhood is changing. They say it feels different. They say it no longer feels like theirs.

Those feelings may be real. Still, beneath many cultural changes is an ownership change.

When ownership changes, the rules of place can change. Price points change. Tenant mixes change. Service priorities change. Security norms change. Design choices change. The assumed customer changes. The imagined future changes.

Culture follows control more often than people admit.

Who Benefits When Value Rises?

Rising neighborhood value is not automatically good or bad.

It depends who benefits.

If local residents own homes, businesses, land, or shares in community assets, rising value can strengthen balance sheets. If they do not, rising value may become rising cost without rising control.

That is the difference between appreciation and displacement.

One builds wealth. The other prices people out of the value they helped create.

This is why ownership timing matters. Waiting until a neighborhood becomes expensive makes ownership harder. By the time outside investors can see the opportunity clearly, local buyers may already be competing against stronger capital.

Ownership has to be built before the market gets obvious.

That requires patience, planning, boring structure, and people willing to buy, hold, maintain, document, and govern assets before applause arrives.

That is not glamorous work. It is the work that keeps a neighborhood from becoming a memory.

The Difference Between Being Served and Being Positioned

A neighborhood can be served without being positioned.

Served means businesses sell products there. Positioned means the community has ownership, influence, and future claims.

Served means needs are met today. Positioned means capacity grows tomorrow.

Served means someone saw a market. Positioned means someone built leverage.

This distinction matters because communities are often told to be grateful for services while being excluded from ownership.

A new store arrives. A new development opens. A new brand enters. A new investor announces improvement.

Some of that may be useful. But the sharper question remains.

What position does the community hold in the new value being created?

If the answer is only customer, worker, renter, or audience, then the structure is incomplete.

Participation is not the same as power.

How Who Owns the Neighborhood Gets Decided

Who owns the neighborhood gets decided through specific actions, not speeches.

Residents learn how property works. Families protect and transfer assets responsibly. Small businesses strengthen books before expansion. Local owners buy buildings when possible. Institutions hold land for long-term use.

In addition, credit unions and mission lenders support viable operators. Merchant groups coordinate instead of competing blindly. Community organizations learn finance, not just advocacy. Developers are judged by structure, not presentation. Public policy protects affordability without destroying maintenance incentives.

None of this is simple.

But simple was never the standard.

The point is durability.

Neighborhood wealth grows when ownership becomes a system rather than a lucky exception.

The Ownership Question Changes the Conversation

Once people ask who owns the neighborhood, the conversation changes.

Complaints become more precise. Strategy becomes more practical. Blame becomes less useful.

People stop treating every visible business as the whole problem and start examining the full structure beneath it.

That is the standard.

A serious economic conversation does not stop at the register.

It looks at land, debt, leases, supply chains, ownership records, institutions, risk, and upside.

That is how a community moves from reaction to strategy.

The Bottom Line

Who owns the neighborhood determines more than who collects rent.

It determines who has leverage when conditions change. It determines who benefits when value rises. It determines who can stay, who can build, and whether money becomes local capacity or temporary motion.

A neighborhood is not only a place.

It is an ownership system.

If that system is invisible, power remains invisible too.

And invisible power is still power.

The Hidden Economy Behind Every Store examines the suppliers, distributors, lenders, landlords, and systems that shape opportunity before the customer ever walks through the door.