Credit scoring systems evaluate you before you ever apply. By the time you request a loan, a card, or a higher limit, the system has already sorted your data, scored your behavior, and positioned your options.

This does not feel dramatic. Instead, it feels administrative. A number appears. A limit appears. A denial appears. However, the real decision happened upstream.

Credit Scoring Systems Start Before Access

Most people think the decision begins when they submit the application. It does not. Credit scoring systems work in advance. They collect signals, organize behavior, and translate financial patterns into institutional judgment.

Payment history, utilization, account age, debt mix, and recent inquiries all move through the structure before any human conversation begins. As a result, access arrives pre-shaped.

This is why system design matters. If the inputs are wrong, the outcome is wrong. If the model is narrow, the result is narrow. The checkpoint does not correct the structure. It reflects it.

Credit Scoring Systems Turn Data Into Limits

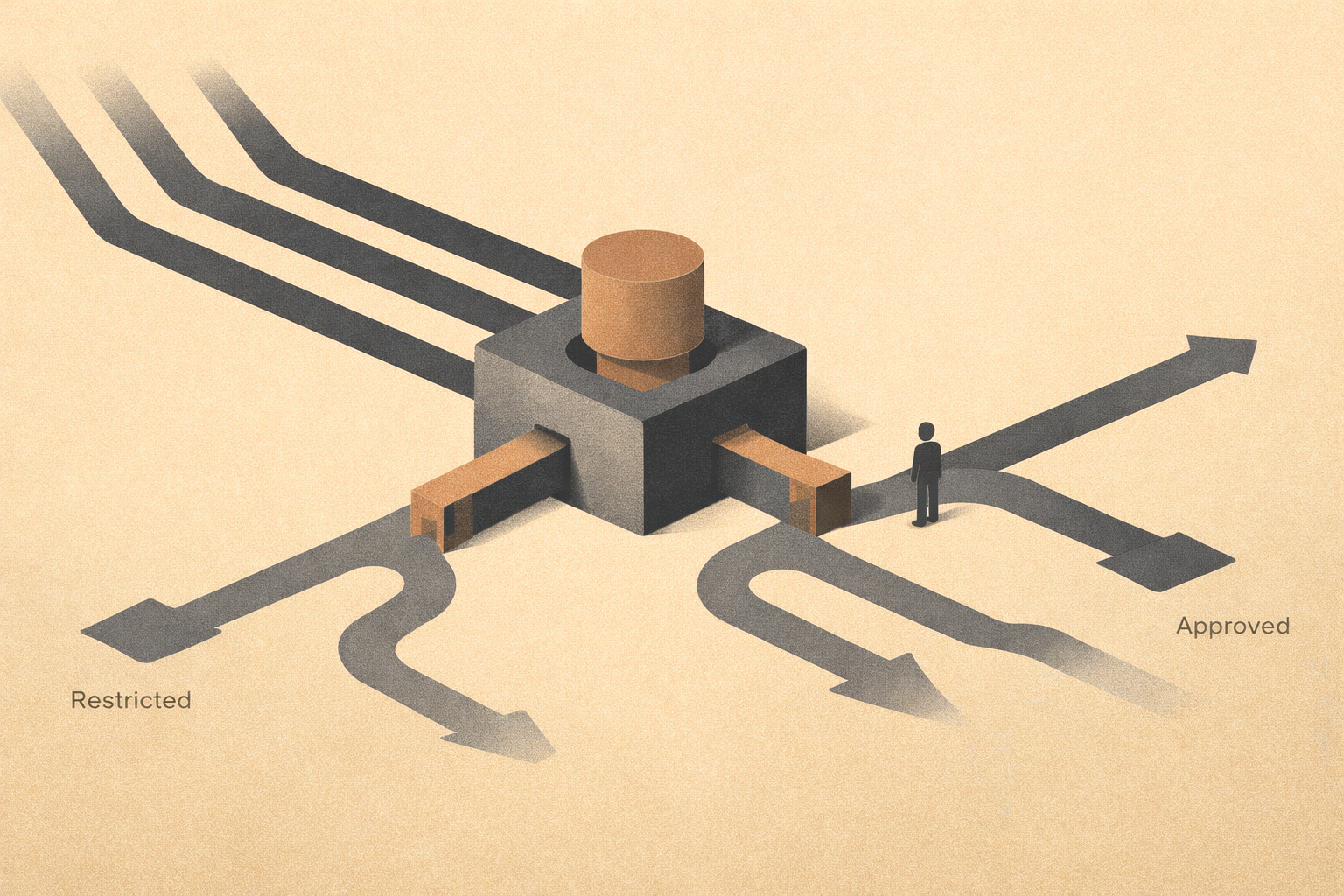

At the center of the process, the system does more than record. It classifies. It places one person closer to approval and another closer to restriction. In other words, it converts behavior into permission.

That conversion feels neutral because it is numerical. Still, numbers can hide power very efficiently. A score does not simply describe risk. It also determines movement.

Approved pathways stay open. Restricted pathways tighten. Some options shrink before the borrower even sees them. Therefore, the system is not just measuring the person. It is shaping the field around the person.

Where Human Review Usually Arrives Too Late

Many institutions still describe the process as balanced because a person can review the file. However, that review often appears after the model has already framed the decision.

The human sees the output, not the full logic. The score has already ranked the applicant. The threshold has already narrowed the range. The review happens inside the system’s conclusion rather than before it.

That is the weakness. A human checkpoint that appears too late is not real control. It is confirmation.

Why Credit Scoring Systems Fail Quietly

These systems rarely fail with noise. Instead, they fail with repetition.

- Incorrect data can remain active longer than it should

- Narrow models can miss context that matters

- Restricted outcomes can appear objective even when the structure is incomplete

Because the process looks orderly, people assume it is fair. Yet structure and fairness are not the same thing. A clean system can still produce distorted outcomes if the model is too rigid or the inputs stay flawed.

For a practical consumer protection lens, the Consumer Financial Protection Bureau explains how errors in credit reporting can be challenged. That matters because contestability is part of accountability.

How to Read the Structure More Clearly

The point is not to panic over scoring. The point is to understand control. Credit scoring systems should support judgment, not replace it entirely.

A stronger structure does three things. First, it records behavior accurately. Second, it evaluates risk with transparent limits. Third, it leaves room for meaningful correction when the model gets something wrong.

This is also why The Structure of Control matters. It names the difference between execution, decision, and authority. Likewise, this lane keeps returning to the same lesson: efficiency without review becomes brittle very quickly.

Credit scoring systems should guide access with discipline. They should not become invisible gatekeepers that nobody can question.

Follow the Tech as Discipline lane from the beginning.

→ The Cost of Convenience: What Automation Removes That You Still Need

→ When Systems Make Decisions for You

→ Designing Friction on Purpose

→ Tech as Discipline: Keeping Humans in the Loop

→ The Structure of Control: Automation, AI, and Human Authority

Tech as Discipline is not interested in speed for its own sake. It is interested in legibility, review, and responsibility. When systems define the path, disciplined people still need a way to question the structure.