How much emergency fund you need depends on your exposure, not a generic rule.

Most people hear the same advice. Save three to six months of expenses. That sounds clear, but it is too vague to apply.

A single income with low obligations carries different risk than a household with dependents, variable income, and fixed costs that cannot pause.

The question is not whether an emergency fund matters. It does. The question is how much protection your situation actually requires.

This decision sits inside the Emergency Fund System, where protection is built, sized, stored, used, and rebuilt with structure.

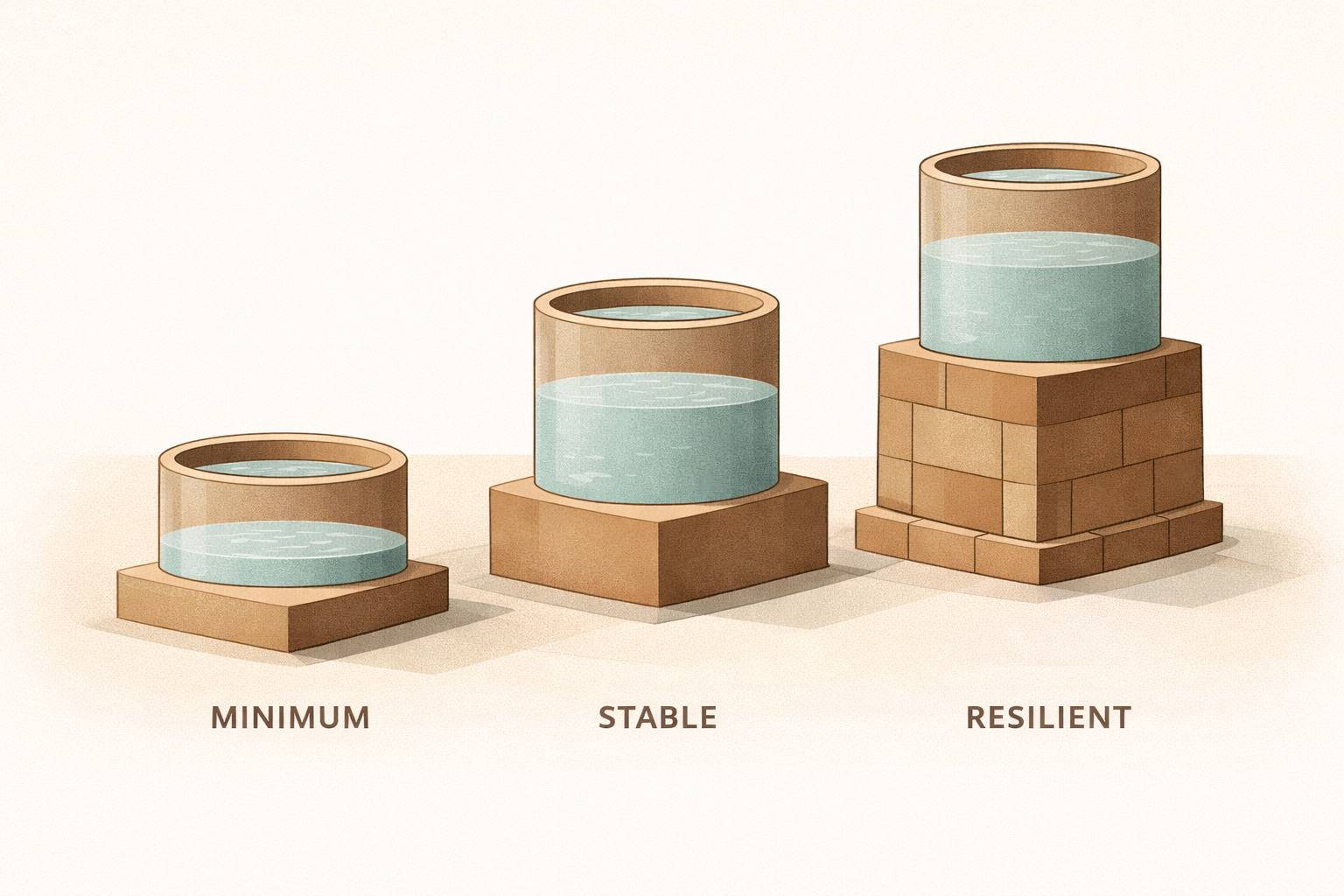

- 1 month = minimum protection

- 3 months = stable baseline

- 6+ months = resilient protection

- Increase reserves as risk increases

What most people get wrong about emergency funds

The mistake is treating all risk as equal.

An emergency fund is not a milestone. It is a buffer against pressure. Its purpose is to absorb disruption before that disruption turns into debt or forced decisions.

Saving toward a random number without understanding exposure leads to two outcomes. People stop too early or delay too long.

Both weaken the system.

How much emergency fund do you need

A better answer uses levels instead of a single target.

Minimum reserve: one month of essential expenses. This protects against short disruptions and prevents small issues from becoming immediate damage.

Stable reserve: three months of essential expenses. This is a practical baseline. It creates room during job gaps, repairs, or unexpected costs.

Resilient reserve: six months or more. This supports households with variable income, dependents, or higher fixed obligations.

This is not about picking a number. It is about selecting a level of protection.

The three emergency fund levels

Each level serves a different function.

- Minimum handles short-term instability

- Stable absorbs moderate disruption

- Resilient protects against longer recovery periods

If income is predictable and obligations are controlled, stable may be enough.

If income fluctuates or others depend on that income, resilient becomes necessary.

How to choose the right emergency fund amount

Use four variables:

- Income stability — how consistent your earnings are

- Dependents — who relies on your income

- Fixed expenses — what must be paid no matter what

- Recovery time — how long it would take to replace income

The more instability in those areas, the larger the reserve should be.

If none of these are defined, the target is guesswork.

This is why Discipline Before Dollars matters. Protection works best when it is structured, not improvised.

If no target number is written down, the emergency fund does not have a defined purpose.

Emergency Fund Quick Calculation

Use this simple method to estimate your emergency fund level.

Step 1: Calculate essential monthly expenses

- housing (rent or mortgage)

- utilities

- food

- insurance

- transportation

- minimum debt payments

Step 2: Multiply based on your risk level

- Low risk: × 3 months

- Moderate risk: × 4 to 5 months

- High risk: × 6+ months

Example:

If your essential expenses are $3,000 per month:

- Minimum protection → $3,000

- Stable reserve → $9,000

- Resilient reserve → $18,000+

The number is not the goal. The level of protection is.

Once your target is clear, the next step is protecting it correctly in Where to Keep Your Emergency Fund So It Actually Works.

When to stop and when to build more

Stop when your current level matches your current exposure.

Build more when the risk increases.

Examples:

- higher housing costs

- new dependents

- shift to self-employment

- increased monthly obligations

As responsibility grows, the reserve should grow with it.

According to the Consumer Financial Protection Bureau, even small emergency savings improve a household’s ability to handle financial shocks.

If no monthly expense number is written down, your emergency fund target is still undefined.

FAQ: Emergency fund size

Is three months enough for an emergency fund?

Three months is a strong baseline for stable income. It may not be enough for variable income or higher responsibility.

Should you aim for six months of expenses?

Six months provides stronger protection, especially for uncertain income or longer recovery periods.

Can you start with less than one month?

Yes. Starting small is better than waiting. The system matters more than the starting amount.

Should your emergency fund increase over time?

Yes. As expenses, responsibilities, or risk increase, the reserve should scale with them.

The Bottom Line

If you are asking how much emergency fund you need, stop looking for a number that fits everyone.

Build the reserve that matches your exposure. Minimum to begin. Stable for breathing room. Resilient when life carries more weight.

The goal is not to save blindly.

The goal is to build enough structure that a hard season does not break the system.

- How to Build an Emergency Fund Without Feeling Broke — Start the reserve

- How to Allocate Money Without Guesswork — Route money with intention

- Discipline Before Dollars — Protect the principle